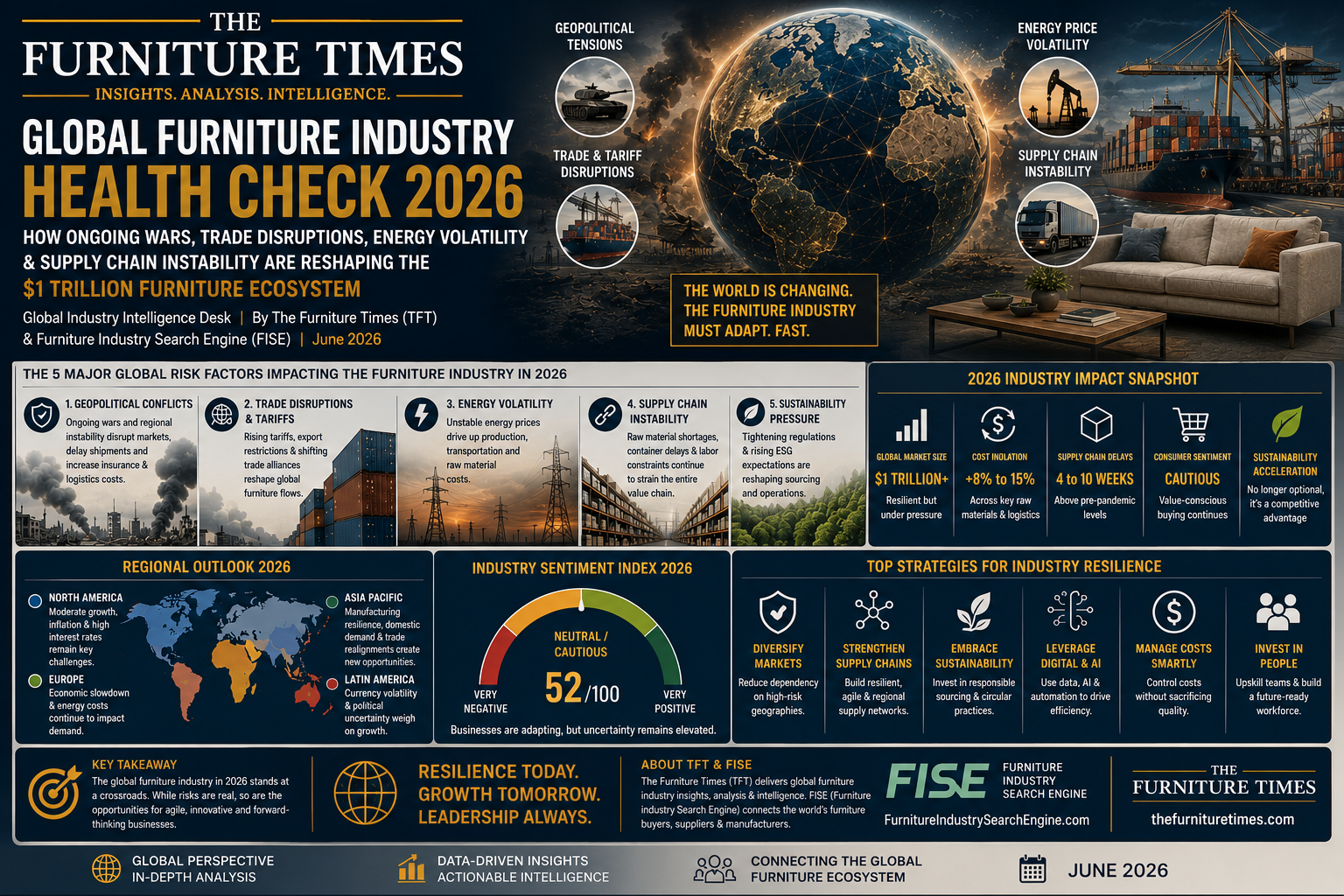

Global Furniture Industry Health Check 2026

How Ongoing Wars, Trade Disruptions, Energy Volatility & Supply Chain Instability Are Reshaping the $1 Trillion Furniture Ecosystem

Global Industry Intelligence Desk | By The Furniture Times (TFT) & Furniture Industry Search Engine (FISE) | June 2026

The global furniture industry finds itself operating in one of the most complex business environments since the COVID-19 era.

Multiple geopolitical conflicts, including the ongoing Russia-Ukraine war, Middle East tensions involving Iran, Israel, and regional actors, Red Sea shipping disruptions, rising energy prices, supply chain uncertainty, and slowing economic growth across several major economies are collectively creating significant pressure on the global furniture ecosystem.

The critical question facing manufacturers, retailers, importers, exporters, suppliers, logistics companies, designers, and investors is simple:

How healthy is the global furniture industry today?

The answer is more complex than many realize.

TFT Global Furniture Industry Health Score

Manufacturing Health

Rating: 7.5/10

Supply Chain Health

Rating: 5.5/10

Consumer Demand Health

Rating: 7/10

Logistics Health

Rating: 5/10

Retail Health

Rating: 6.5/10

Investment Health

Rating: 7/10

Global Industry Health Score

Overall Rating: 6.4/10

The industry remains resilient, but significant stress points continue to emerge.

War Zone Impact Analysis

Russia–Ukraine War

More than four years into the conflict, its effects continue to ripple through global manufacturing and trade.

The furniture industry has experienced impacts through:

Timber supply volatility

Rising energy costs

Higher transportation expenses

Inflationary pressure

Reduced consumer spending power in parts of Europe

European manufacturers remain particularly exposed to elevated operating costs compared to pre-war conditions.

Middle East Conflict

The Middle East has become the largest risk factor for global furniture supply chains in 2026.

The ongoing tensions involving Iran, Israel, regional shipping lanes, and the Red Sea have created significant uncertainty across international logistics networks.

Why This Matters To Furniture

Furniture products are:

Large

Heavy

Container-dependent

Freight-sensitive

Unlike electronics or luxury goods, furniture margins can be significantly affected by shipping costs.

When shipping routes are disrupted, furniture companies often feel the impact quickly.

The Red Sea Problem

The Red Sea remains one of the world’s most important trade corridors.

Shipping disruptions continue to affect global supply chains, particularly between Asia and Europe. Traffic remains below pre-conflict levels, and further escalation risks additional rerouting.

For furniture companies this means:

Longer transit times

Higher insurance costs

Increased inventory requirements

Delayed deliveries

Reduced cash-flow efficiency

Industry research has shown furniture retailers are among the sectors heavily exposed to Red Sea shipping disruptions, particularly in Europe.

Oil Prices: The Silent Threat

Furniture manufacturers may not sell oil.

But they consume its effects every day.

Oil influences:

Transportation

Foam production

Plastics

Packaging

Chemicals

Adhesives

Logistics

Recent geopolitical tensions have pushed oil prices higher and increased concerns regarding energy stability.

Higher energy costs eventually affect:

Furniture factories

Container shipping

Warehouse operations

Raw material suppliers

The Supply Chain Health Check

The good news:

Global supply chains have not collapsed.

The concern:

They remain fragile.

The New York Federal Reserve’s Global Supply Chain Pressure Index indicates continued elevated pressure levels linked to geopolitical disruptions and trade uncertainty.

Many companies have responded by:

Diversifying suppliers

Building inventory buffers

Nearshoring production

Increasing regional sourcing

Winners Emerging From The Crisis

Not every country is losing.

Several furniture-producing nations are strengthening their position.

Vietnam

Continuing to attract international sourcing.

Indonesia

Growing manufacturing investment.

India

Expanding export opportunities.

Malaysia

Benefiting from diversification strategies.

Mexico

Strengthening nearshoring opportunities for North America.

These countries are increasingly viewed as strategic alternatives within global furniture supply chains.

Furniture Retail Health Check

Retail performance remains mixed.

Strong Segments

Luxury furniture

Hospitality furniture

Outdoor furniture

Commercial furniture

Custom manufacturing

Under Pressure

Mid-market retailers

Import-dependent retailers

Businesses with weak digital visibility

Several furniture retailers and brands have recently entered liquidation or closed operations, highlighting ongoing pressure within the retail sector. Consumer confidence remains uneven across regions.

The Rise of the Visibility Economy

One trend continues to accelerate regardless of conflict:

Digital discoverability.

Customers increasingly discover furniture suppliers through:

Search engines

AI assistants

Digital directories

Online reviews

Social platforms

The industry is moving toward what TFT and FISE call the Visibility Economy, where discoverability directly influences commercial opportunity.

Businesses with strong visibility continue generating leads even during market uncertainty.

What Keeps CEOs Awake in 2026?

Furniture executives globally identify several key risks:

Rising Costs

Materials, energy, and labor remain volatile.

Supply Chain Uncertainty

Shipping routes remain vulnerable.

Consumer Demand Fluctuation

Economic uncertainty affects discretionary spending.

Trade Fragmentation

Geopolitical tensions continue reshaping global trade patterns.

Talent Shortages

Manufacturing labor remains difficult to secure in many markets.

The Furniture Industry Risk Map

High Risk

Red Sea shipping exposure

Energy-intensive manufacturing

Single-source supplier dependency

Medium Risk

European retail markets

Long-haul export models

Commodity-driven furniture categories

Lower Risk

Regional manufacturing ecosystems

Diversified sourcing models

High-value custom furniture

Hospitality and project-based businesses

TFT Forecast: 2026–2028

The Furniture Times Global Intelligence Team expects:

Scenario 1: Controlled Stabilization (Most Likely)

Gradual supply chain recovery

Moderate freight stabilization

Steady furniture demand growth

Probability: 55%

Scenario 2: Extended Conflict Disruption

Continued shipping volatility

Higher energy prices

Margin pressure

Probability: 30%

Scenario 3: Rapid Recovery

Reduced geopolitical tensions

Lower freight costs

Stronger global consumer confidence

Probability: 15%

Final Verdict

Despite wars, geopolitical tensions, logistics disruptions, and economic uncertainty, the global furniture industry remains remarkably resilient.

The industry is not facing collapse.

It is facing transformation.

Manufacturers are adapting.

Supply chains are evolving.

Buyers are changing.

Technology is accelerating.

The winners of the next decade will not simply be the largest furniture companies.

They will be the most adaptable, most resilient, most visible, and most discoverable.

In times of uncertainty, industries do not disappear.

They reinvent themselves.

The global furniture industry’s health score of 6.4/10 indicates caution, not crisis.

The ecosystem remains under pressure, but the foundations of global furniture demand, housing growth, urbanization, hospitality expansion, and manufacturing innovation remain intact.

By The Furniture Times (TFT) & Furniture Industry Search Engine (FISE)

Global Industry Intelligence Desk | June 2026

“TFT tells their story. FISE helps the world find them.”