Qatar Furniture Market Impact from the Iran–U.S.–Israel War: Deep Analysis of Disruption, Losses, and Ecosystem Risk

The Furniture Times

The Qatar furniture industry is facing a serious geopolitical stress test as the Iran–U.S.–Israel war disrupts trade routes, raises shipping risk, and weakens confidence across the Gulf business environment. For Qatar, the danger is not only political or energy-related. It is commercial, logistical, operational, and structural. The furniture ecosystem is especially exposed because it depends heavily on imported products, imported materials, international shipping reliability, and the continuous health of real estate, hospitality, retail, and fit-out demand. Reuters has reported that traffic through the Strait of Hormuz has been repeatedly disrupted during the conflict, with commercial shipping uncertainty, gunfire incidents involving merchant vessels, and renewed warnings to mariners. Reuters also reported war-risk insurance surges that in some cases exceeded 1,000% during the crisis.

This matters deeply to Qatar because the country’s wider economy and business confidence are tied to Gulf logistics stability. Reuters reported that the conflict, which began on February 28, 2026, has already affected Qatar’s LNG operations and reduced capacity at Ras Laffan after Iranian attacks, while Gulf equity markets, including Qatar’s, have shown stress linked to Hormuz uncertainty. Even when temporary reopening signals appeared, shipping companies reportedly still sought clarification before fully resuming transit, showing that “open” does not mean “normal.”

For the furniture sector, the first major impact is supply-chain disruption. Qatar imports far more furniture than it exports. OEC shows Qatar imported about $588 million in “Furniture, bedding, lamps, and prefab buildings” in 2024, with a net trade deficit of roughly $585 million in that category, underscoring heavy external dependence. World Bank WITS data also shows Qatar imported over $45 million in wooden bedroom furniture alone in 2024, led by suppliers including China, Turkey, Italy, Malaysia, and Vietnam. That means any shock to sea freight, transshipment, insurance, or delivery schedules quickly reaches showrooms, project suppliers, interior contractors, hotels, offices, and residential buyers in Qatar.

The second impact is cost inflation across the furniture value chain. When maritime war-risk premiums spike, freight prices rise, cargo delays increase, and suppliers begin adding buffers, surcharges, or stricter payment terms. Reuters reported that war-risk premiums rose from around 0.25% to as high as 3% of a vessel’s value in the conflict, with risky-zone definitions extending beyond the Strait itself. For the furniture industry, this is painful because many items are bulky, margin-sensitive, and time-dependent. A sofa, wardrobe system, office workstation package, hotel FF&E consignment, or custom joinery cargo delayed at sea does not only cost more to transport; it can also trigger project penalties, storage issues, labor rescheduling, and lost sales windows.

The third impact is project execution risk. Qatar’s real estate and hospitality sectors are important demand engines for furniture. Invest Qatar says the country’s real estate sector has been supported by large-scale construction investment, including $250 billion in construction projects, while Qatar Tourism’s 2025 annual report says the country welcomed 5.1 million international visitors, hotel supply reached about 42,469 keys, and room demand rose 8.6% in 2025. Those are strong fundamentals for furniture demand in homes, hotels, serviced apartments, restaurants, offices, and mixed-use projects. But when war disrupts logistics, the furniture ecosystem suffers through delayed handovers, postponed fit-outs, slower procurement cycles, and cautious capital spending.

The fourth impact is inventory distortion. In normal conditions, import-reliant furniture markets can run on predictable lead times. In conflict conditions, buyers often react in two opposite ways: some delay purchasing because of uncertainty, while others rush to secure stock before costs climb further. That creates an unstable market where some businesses face stock-outs and others get trapped in high-cost inventory that moves too slowly. This effect is especially dangerous for premium furniture, hospitality supply, custom-made interiors, and office projects where product specification matters and substitutes are limited. This loss pattern is an inference from the shipping and import facts above, but it is a commercially reasonable one given Qatar’s dependence on imported furniture and the current disruption to Gulf shipping.

The fifth impact is pressure on retail and consumer demand. Even if Qatar remains relatively stable domestically, sustained regional conflict can weaken business sentiment, delay relocation decisions, soften discretionary luxury purchases, and make both households and firms more price-conscious. Reuters reported continuing uncertainty in Gulf markets tied to Hormuz risks and U.S.-Iran negotiations. In furniture, that can reduce conversion rates for premium residential purchases, imported décor, and non-essential upgrades, while shifting demand toward value products, ready stock, and faster-delivery alternatives.

The sixth impact is loss to the wider furniture ecosystem, not just sellers of finished products. The Qatar furniture market includes importers, distributors, retailers, fit-out firms, carpentry workshops, interior designers, project consultants, logistics providers, warehousing partners, installers, after-sales teams, online furniture sellers, and hospitality procurement specialists. When geopolitical disruption intensifies, the damage spreads across the ecosystem in layers:

first freight and insurance,

then landed cost,

then project timing,

then retail confidence,

then cash flow,

then hiring,

then expansion plans.

This cascading effect is why wars often hurt furniture ecosystems more broadly than headline sales data initially shows. The ecosystem loss is therefore not only direct revenue loss; it is also lost speed, lost margins, lost confidence, and lost growth momentum. This is an inference based on the reported shipping, insurance, and demand-channel risks.

Where Qatar’s furniture industry may lose the most

The most exposed segments are likely to be:

1. Hospitality furniture and fit-out

Hotels, serviced apartments, F&B venues, and tourism-linked projects depend on installation timelines and imported product consistency. Qatar Tourism’s 2025 data shows the hospitality base is large and active, so delays here can have outsized project impact.

2. Premium imported residential furniture

Luxury and branded products sourced from overseas become vulnerable to freight spikes, inventory gaps, and postponed consumer spending.

3. Office and commercial interiors

Corporate caution during geopolitical stress can delay workspace upgrades, expansions, and procurement cycles. This point is an inference from the broader market-risk environment and project timing pressures.

4. Small and mid-sized furniture traders

Larger companies may absorb delays better; smaller firms often suffer more from cash-flow strain, slower stock turnover, and advance-payment pressure from overseas suppliers. This is an inference, but it is consistent with the reported rise in shipping and insurance costs.

How big could the loss be?

There is no reliable public source yet that quantifies the exact dollar loss to Qatar’s furniture industry from this war alone, so any precise figure would be speculation. What can be said with confidence is that an import-dependent market of this kind is vulnerable to three measurable forms of loss:

- Margin loss from higher freight, insurance, and handling costs.

- Revenue loss from delayed projects, delayed showroom conversion, and deferred purchases. This is an inference supported by the shipping disruption and business uncertainty.

- Ecosystem loss from slower market velocity across hospitality, retail, real estate fit-out, and furniture services.

A practical reading is this: if Hormuz instability continues, the Qatar furniture ecosystem may not collapse, but it can enter a period of compressed margins, slower deal flow, higher working-capital pressure, and delayed sector expansion. That is often how industry loss appears before it shows up in official annual statistics.

Strategic conclusion

The Iran–U.S.–Israel war is not a distant geopolitical headline for Qatar’s furniture market. It is a direct stress factor on the ecosystem’s logistics, imports, pricing, timelines, confidence, and growth pipeline. Qatar still has strong underlying demand drivers through real estate, hospitality, and national development strategy, but the furniture market’s dependence on imported goods makes it especially vulnerable in a prolonged Gulf shipping crisis. The deepest loss may not be one dramatic number. It may be the combined effect of delayed cargo, rising landed cost, project slowdowns, weaker purchasing confidence, and reduced expansion across the entire furniture value chain.

Related Posts

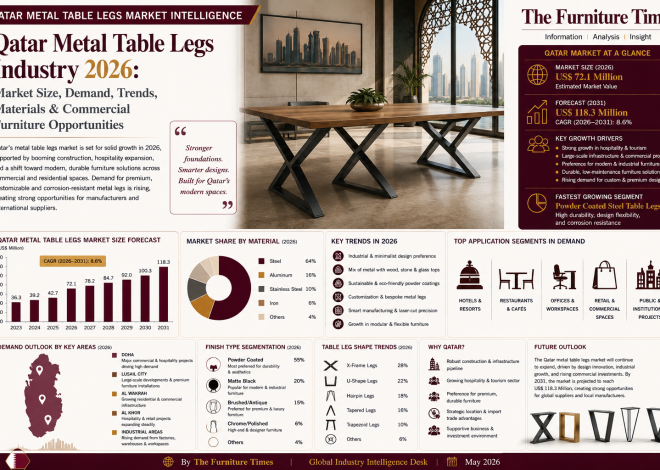

Qatar Metal Table Legs Industry 2026: Market Size, Demand, Trends, Materials & Commercial Furniture Opportunities

Qatar Furniture Market Under Pressure as Iran–U.S.–Israel War Disrupts Gulf Trade Arteries